The story dominating tech media right now is the AI bubble. The evidence, at first glance, looks damning:

- Uber burned through its entire 2026 AI budget in four months.

- Microsoft abruptly canceled its internal Claude Code pilot after costs spiraled.

- GitHub couldn't keep up with demand for Copilot and had to freeze new sign-ups.

- AI software prices jumped 20-37% across the board.

Critics are calling it the near end of the AI Bubble.

We read the same headlines, but we came to different conclusions.

What do we know so far?

Eight data points dominate the conversation. On the surface, they paint a picture of an industry in crisis.

Dig one layer deeper, and each tells a different story.

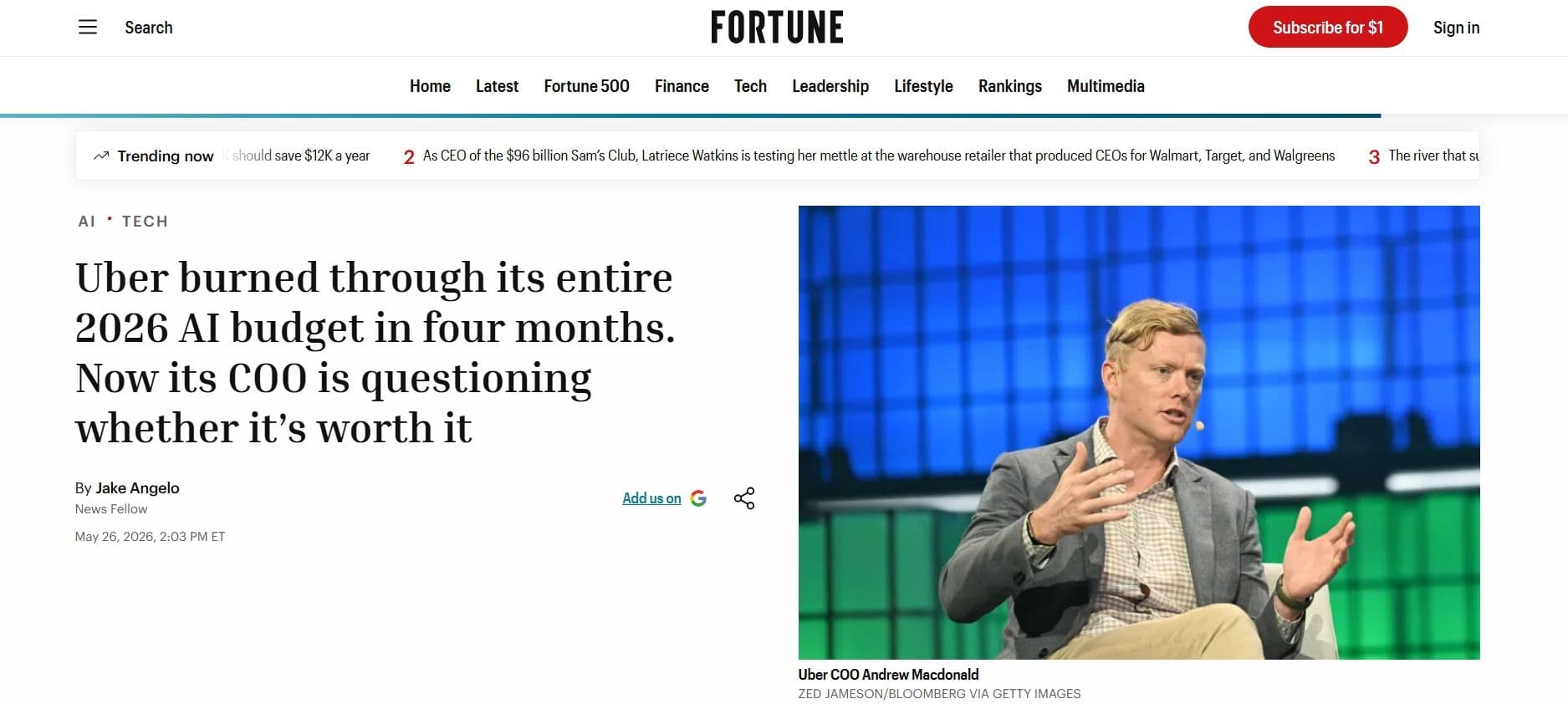

1. Uber Exhausted a Full Year's AI Budget in Four Months

In April 2026, Uber CTO Praveen Neppalli Naga fired off an internal memo that ricocheted through Silicon Valley: the company had spent its entire 2026 AI allocation by the end of Q1. Four months.

Uber's demand for AI is running so far ahead of even aggressive forecasts that annual budgets have become meaningless.

But here’s something unseen: this isn't a company retreating from AI. It's a company that has already committed $3.4 billion to AI infrastructure and is actively reallocating, not reducing.

When a company blows through a budget this fast, it means one thing: actual usage exceeds expectations. That's usage proof that AI was actually doing the work.

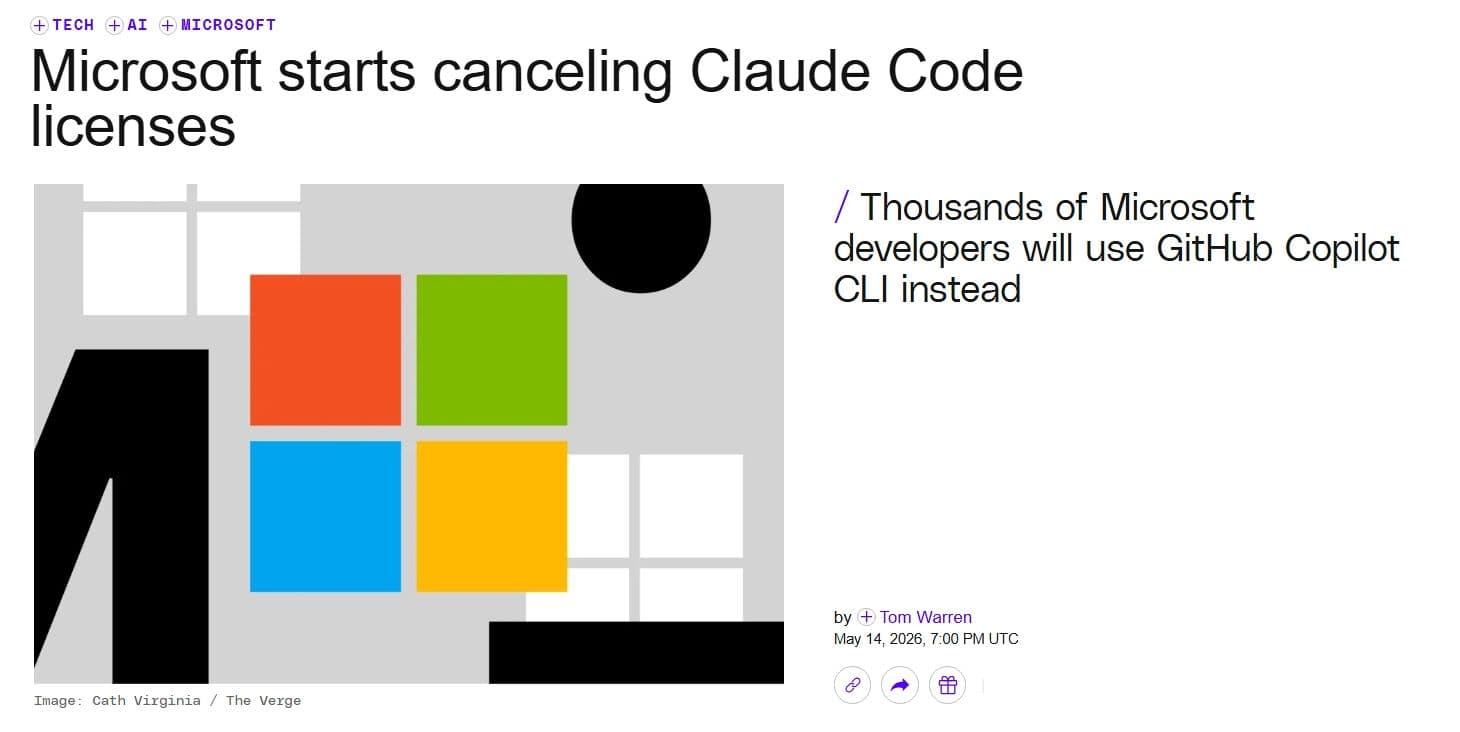

2. Microsoft Killed Its Internal Claude Code Licenses

In May 2026, Microsoft began canceling internal Anthropic Claude Code licenses across its Experiences + Devices division, the teams behind Windows, Microsoft 365, Outlook, Teams, and Surface.

Token-based billing made Claude Code "too costly to manage at scale." Thousands of developers who have integrated Claude Code into their daily workflows since December 2025 are being moved to GitHub Copilot CLI by June 30.

The pilot was cancelled because it was too popular. Internal adoption spread faster than the procurement team could budget for.

Microsoft effectively ran a six-month bakeoff between Anthropic and its own tooling and decided ownership plus cost control mattered more.

3. GitHub Froze Copilot Sign-Ups and Killed Flat-Rate Pricing

In April-May 2026, GitHub suspended new sign-ups for Copilot Pro, Pro+, and Student plans. The official reason: "Agentic coding workflows are now routinely generating costs that exceed what users pay per month." Flat-rate subscriptions were being driven to bankruptcy by actual developer consumption.

GitHub pivoted to usage-based "AI Credits" billing, scrapping the model that had powered its growth for years.

Users are using Copilot so much that the old pricing model broke. That's the opposite of a collapse in demand. Its demand exceeds the system's ability to charge for it. GitHub isn't losing customers. It's fixing a pricing model that was too generous.

4. Global AI Spending Is Projected at $2.59 Trillion in 2026

Gartner published its AI spending forecast on May 19, 2025. The numbers:

2025

- Global AI Spending: $1.76 trillion

2026

- Global AI Spending: $2.59 trillion

- Growth: $+47\%$ Year-over-Year (YoY)

2027

- Global AI Spending: $3.49 trillion

- Growth: $+98\%$ increase compared to 2025 levels

Gartner's analysts noted this is "dominated by vendors and hyperscalers, with enterprises yet to flex spending potential." The next wave of spending, from every company that isn't a tech giant, hasn't even hit yet.

5. Hyperscalers Are Planning $700 Billion in AI Capex for 2026

Amazon: $44.2 billion in quarterly capex. Google: $35.67 billion per quarter, more than double year-over-year. Google Cloud's backlog alone now exceeds $460 billion. Meta and Microsoft are on similarly aggressive trajectories.

The combined hyperscaler AI infrastructure spend is approaching $700 billion for 2026.

These aren't companies known for charitable donations to the GPU industry. They're building infrastructure for a consumption wave that hasn't crested.

6. SpaceX Is Acquiring AI Developer Tool Cursor

In May 2026, SpaceX, a rocket and satellite manufacturing company, secured the right to acquire Cursor, one of the most popular AI-native developer tools.

A company that builds rockets is buying a coding AI startup. Developer AI tools have become strategic assets for non-software companies. That's not a signal of a dying market. It's a signal that AI-powered development is being treated as infrastructure as essential as the machines on the factory floor.

(Notably, Microsoft reportedly looked at acquiring Cursor first but didn't make an offer.)

7. McKinsey Deployed 25,000 AI Agents Alongside 60,000 Employees

In January 2026, McKinsey CEO Bob Sternfels announced the firm now operates 25,000 AI agents alongside 60,000 human employees. His stated goal: every employee working alongside an AI agent within 18 months.

This is the consulting firm Fortune 500 companies pay millions to for strategic advice, betting its own operations on AI agents at scale. If McKinsey is wrong about this, the consequences are more meaningful than a bad quarterly earnings call.

So What's Actually Happening?

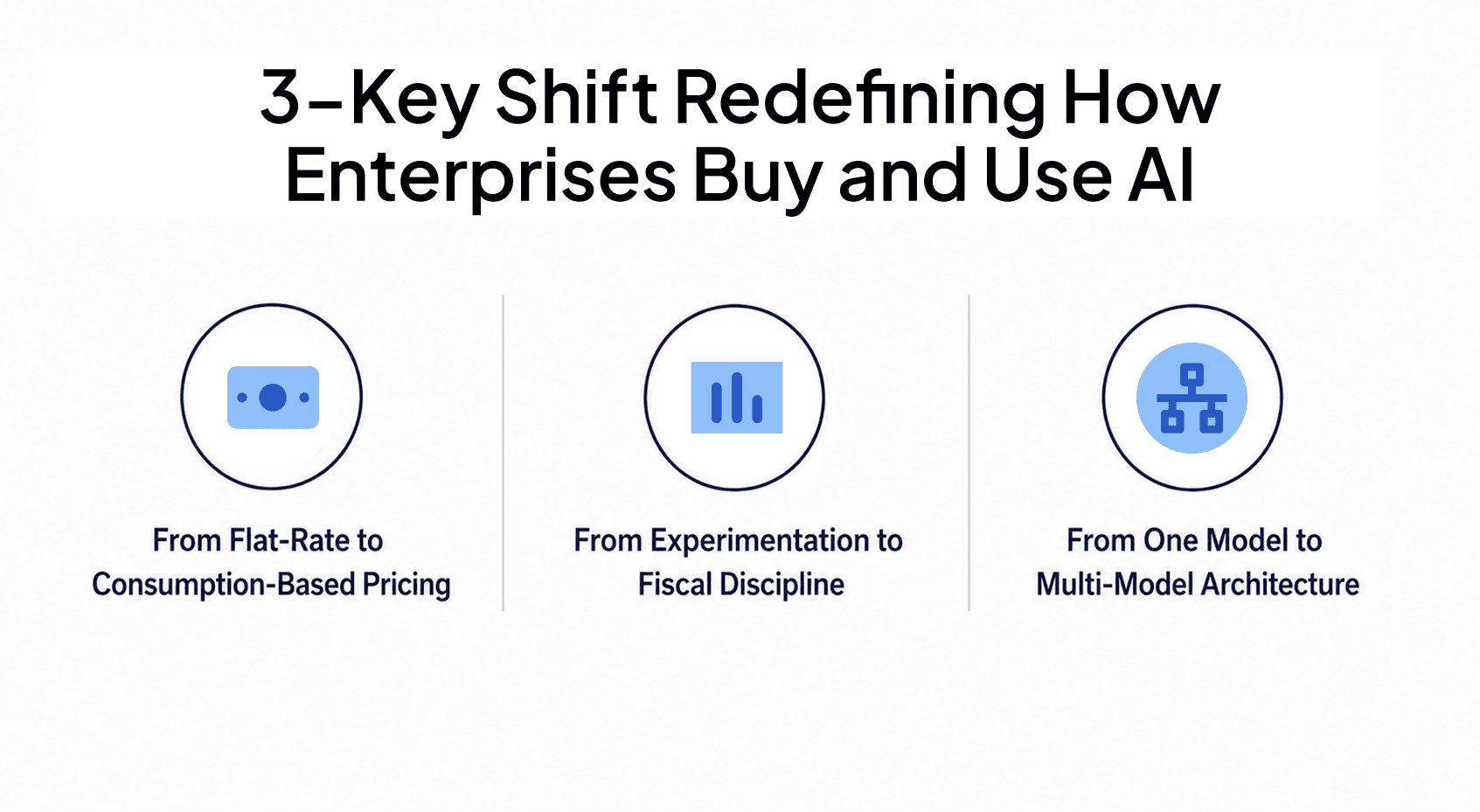

None of these signals points to retreat. They point to three structural changes happening simultaneously:

Change 1: From Flat-Rate to Consumption-Based Pricing

The subscription era of AI is ending. GitHub, Anthropic, OpenAI, and every major provider are or will be moving to usage-based billing. When you charge by the token, heavy users can drain budgets faster than finance departments can track them, as Uber and Microsoft learned.

If you are an enterprise, you can check out our latest write-up to learn more about it here.

Change 2: From Experimentation to Fiscal Discipline

For two years, enterprises threw money at AI tools to see what stuck. That phase is over. CFOs are now looking at token receipts, questioning productivity-per-dollar, and demanding ROI. This looks like a retrenchment to outsiders. To anyone inside enterprise IT, it's business as usual after any technology hype cycle.

AI budgets being scrutinized don't mean they're being cut. It means they're being allocated intelligently.

Change 3: From One Model to Multi-Model Architecture

Businesses are realizing that using the most powerful model for every task is unsustainable. Organizations are following the known trick in the book of AI: frontier models for complex reasoning, cheaper models for routine work. This fragmentation is going to accelerate.

That's why cheaper open-source models are becoming the ones consuming more than 2.35 trillion tokens weekly in Open Router.

Microsoft's move from Claude Code to Copilot CLI isn't about choosing one model forever. Claude models remain accessible through Copilot. What's changing is the control layer, the interface through which employees access AI and how costs are managed.

The Price Collapse No One's Talking About

While everyone fixates on runaway costs, the biggest story in AI is largely being ignored: frontier model pricing is changing.

On May 23, 2026, DeepSeek made its 75% discount on the V4 Pro model permanent.

Here's what the pricing landscape now looks like:

GPT-5.5 (OpenAI)

- Input Cost: $15.00 per 1M tokens

- Output Cost: $30.00 per 1M tokens

- Comparison: Baseline ($1\times$)

Claude Opus 4.7 (Anthropic)

- Input Cost: $15.00 per 1M tokens

- Output Cost: $75.00 per 1M tokens

- Comparison: $2.5\times$ more expensive than GPT-5.5 output

Claude Sonnet 4.6

- Input Cost: $3.00 per 1M tokens

- Output Cost: $15.00 per 1M tokens

- Comparison: $0.5\times$ the cost of GPT-5.5 output

Gemini 3.1 Pro (Google)

- Input Cost: $3.50 per 1M tokens

- Output Cost: $10.50 per 1M tokens

- Comparison: $0.35\times$ the cost of GPT-5.5 output

Gemini 3.5 Flash

- Input Cost: $0.15 per 1M tokens

- Output Cost: $0.60 per 1M tokens

- Comparison: $50\times$ cheaper than GPT-5.5 output

DeepSeek V4 Pro

- Input Cost: $0.435 per 1M tokens

- Output Cost: $0.87 per 1M tokens

- Comparison: $34.5\times$ cheaper than GPT-5.5 output

DeepSeek V4 Flash

- Input Cost: $0.07 per 1M tokens

- Output Cost: $0.28 per 1M tokens

- Comparison: $107\times$ cheaper than GPT-5.5 output

DeepSeek V4 Pro Preview, a 1.6 trillion parameter model that comes close to GPT-5.5 on coding benchmarks (80.6% on SWE-bench Verified vs. 82.1%, and 93.5% on LiveCodeBench vs. 91.8%), now costs $0.87 per million output tokens.

At that price, an autonomous coding agent session (500K input + 100K output) costs $0.31. On Claude Opus 4.7, the same session costs $26.25. That's an 85× difference.

And this isn't promotional pricing with an expiration date. DeepSeek explicitly removed the deadline. Running on Huawei Ascend 950 chips gives them sustainable unit economics that Western providers, dependent on NVIDIA silicon, cannot currently match.

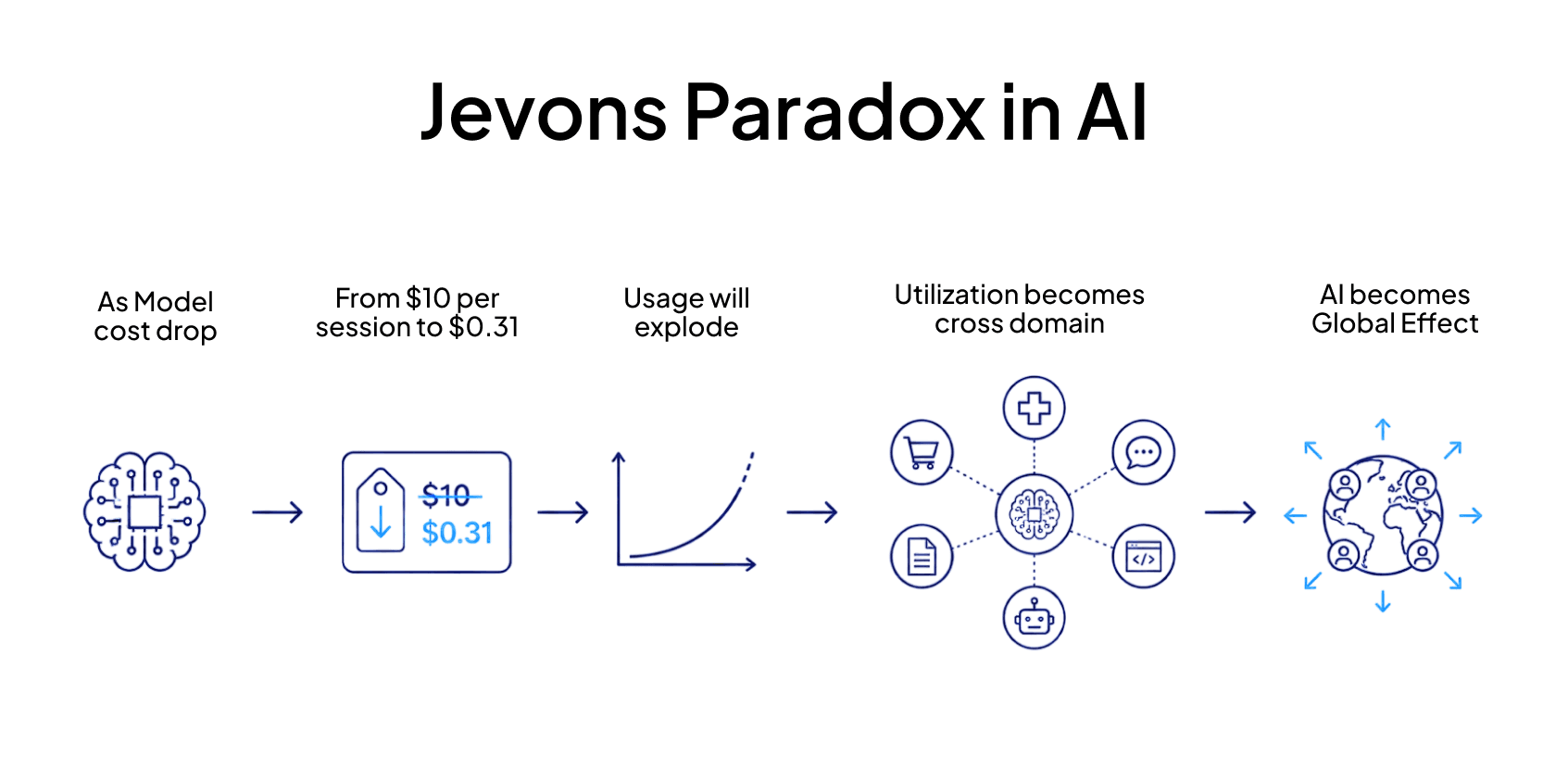

Jevons Paradox in Action

In 1865, economist William Stanley Jevons observed that improvements in coal efficiency didn't reduce coal consumption. They dramatically increased it because cheaper coal unlocked entirely new uses.

AI is heading for the same dynamic. When AI reasoning drops from $10 per session to $0.31, demand doesn't stay flat. It explodes into domains and use cases that were previously cost-prohibitive. Every dollar of infrastructure capex suddenly goes dramatically further, which means more consumption, not less.

Consider the real-world math: a RAG pipeline processing 1,000 queries per day costs $39/month on DeepSeek V4 Pro. The same workload on GPT-5.5 costs $1,350/month. That 34× delta doesn't just save money. It creates entirely new addressable markets.

What Enterprises Should Actually Learn From All of This

1. Demand Is Real, the Challenge Is Governance

AI adoption is moving faster than AI governance. When companies like Uber and Microsoft struggle to budget for AI costs, the problem is not that AI isn't delivering value. It's that procurement, finance, and IT governance haven't caught up to consumption patterns that look nothing like traditional SaaS.

The enterprises that thrive through this shift will be the ones that build internal frameworks for: tracking AI tool usage across teams, matching model capability to task complexity, and treating AI spend as a strategic line item rather than a departmental afterthought.

2. You Cannot Bet on One Model

A model that works well today may become too expensive tomorrow. Another model may become better for a specific use case. Pricing will change. Capabilities will shift. Security and compliance requirements will evolve.

The organizations building AI strategy around a single vendor are the ones most exposed. The winners will architect for model flexibility: using frontier models for complex reasoning, efficient models for routine tasks, and maintaining the ability to switch without rebuilding everything.

3. The Moat Is Shifting

As model costs collapse toward zero, the competitive advantage shifts from which model you have access to toward:

- Workflow integration: How well AI fits into CI/CD, operations, and business processes

- Orchestration and governance: Controlling which models are used for which tasks, with what guardrails

- Evaluation and quality gates: Measuring AI output against business outcomes, not just tokens consumed

- Domain customization: Fine-tuning, few-shot learning, and tool use specific to your business

The bottleneck is no longer cost. It's organization.

So What Does This Mean

The AI bubble narrative is not entirely false, but it mistakes a repricing event for a collapse.

What's actually happening: the industry is moving from enthusiastic-but-inefficient flat-rate adoption to disciplined, consumption-based deployment. It's messy. It's producing uncomfortable headlines. But it's the same maturation arc every transformative technology has followed: from mainframes to personal computers, from on-prem to cloud, and now from experimental AI to operational AI.

Enterprise budgets are being blown through because usage is real. Pricing models are breaking because demand exceeds them. Hyperscalers are investing $700 billion because they see the consumption wave coming. Frontier models are collapsing in price because competition is working.

The enterprises that haven't even started spending yet? That's $3.49 trillion waiting to happen.

The real buildout is just beginning.